Introduction to Annuities

With 60% of people concerned they might outlive their retirement resources, annuities can provide the guaranteed1 income that 99% of savers say would help them feel secure2.

Let’s break down a few annuity essentials: what are they, who they are for, and which one is right for you?

Distinct Types of Annuities

Fixed Indexed Annuity

Variable Annuity3

Registered Index Linked Annuity4

(RILAs) offer the potential for higher growth linked to market performance with partial downside protection.

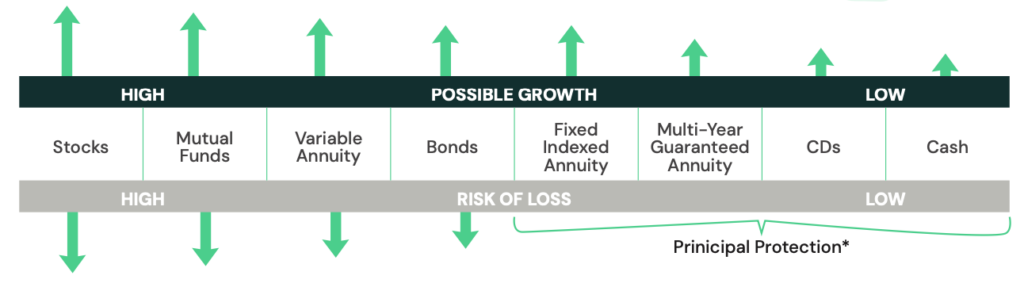

How do annuities compare with other options?

| Features | Annuities | IRAs | CDs | Muni Bonds | Govt. Bonds | EE Bonds |

|---|---|---|---|---|---|---|

| Tax Deferral | Yes | Yes | No | N/A | No | Yes |

| Tax-Free | No | No | No | Yes | No | No |

| Tax-Deductible | No | Yes | No | No | No | No |

| Market Risk | No | Yes | No | Yes | Yes | No |

| Safety of Principal | Safe | Varies | Safe | Varies | Safe | Safe |

| Surrender Charge(s) on Early Withdrawal | Based on Contract | Possible back-end sales charge | Penalties | None | None | Moderate |

| Tax Penalties on Early Withdrawal | Possibly Harsh | Possibly Harsh | None | None | None | None |

How risky Are annuities?

How do i get an annuity?

Discuss

Talk to your financial professional about your goals and needs in retirement.

Research

Choose a reputable insurance carrier with a strong financial rating, like United Life Insurance Company.

Select

Select the type of annuity that will help with your individual financial goals.

Purchase

Work with your financial professional to purchase an annuity from United Life.

Dive deeper into annuities

Frequently Asked Questions

Check out our Glossary of Terms for help in understanding industry definitons.

What is a tax-deferred annuity?

A tax-deferred annuity lets your savings grow without being taxed until you withdraw the funds, usually during retirement. This can help you accumulate more over time, since your earnings are not reduced by taxes each year.

Is a tax-deferred annuity a good idea?

Is an annuity the same as a 401(k)?

How does a deferred annuity work?

Are there disadvantages to tax-deferral?

One potential disadvantage of tax-deferred annuities is that while you defer taxes on earnings until you take the money out, you may end up paying higher taxes later if your tax rate increases in retirement. Additionally, early withdrawals before age 59½ may have a 10% penalty from the IRS.

Are annuities good products?

What are the downsides of annuities?

Who is the right fit for an annuity?

Annuities are best suited for individuals looking for a guaranteed* income stream in retirement, those who want to manage longevity risk and those seeking tax-deferred growth. They can be particularly beneficial for more conservative people who want financial security over higher returns.

*Annuity Guarantees rely on the financial strength and claims-paying ability of the issuing insurer.

Who should not buy an annuity?

Individuals who need immediate liquidity, prefer high-growth investments, or have a short investment horizon should not buy an annuity. Additionally, those uncomfortable with the fees and complexities associated with annuities may want to explore other financial options.

What is the right age to own an annuity?

The ideal age to buy an annuity depends on your personal financial situation, but many people consider purchasing one in their 50s or 60s when they are approaching retirement and looking to secure a guaranteed* income stream without risking their savings directly in the market.

*Annuity Guarantees rely on the financial strength and claims-paying ability of the issuing insurer.

How much does an annuity pay per month?

Where can I get an annuity?

You can buy an annuity through insurance companies, financial advisors, banks, and online financial platforms. It’s important to compare options and seek advice from a trusted financial professional to find the best annuity for your needs. All annuities are issued by insurance companies.

Is an annuity the same as an IRA (Individual Retirement Account)?

No, they are not the same. An annuity is an insurance product designed to provide a guaranteed* income stream, often in retirement. An IRA, on the other hand, is a tax-advantaged retirement savings account. That said, it is possible to hold an annuity within an IRA as part of your overall retirement strategy.

*Annuity Guarantees rely on the financial strength and claims-paying ability of the issuing insurer.

How do I make money with an annuity?

Annuities generate earnings through interest or investment growth on your initial contribution, depending on the type you choose. Fixed annuities offer guaranteed* interest, while variable and indexed annuities tie their returns to market performance or a specific financial index. These earnings grow tax-deferred, allowing your investment to compound over time until you begin making withdrawals.

*Annuity Guarantees rely on the financial strength and claims-paying ability of the issuing insurer.

Are annuities expensive?

The price of an annuity depends on several factors, including the type of annuity, your initial investment amount, and any optional features such as riders you choose to add. You can generally purchase an annuity with a lump sum ranging from $10,000 to over $1 million.

While many fixed annuities have no fees, especially those with added benefits, may include ongoing charges that vary based on the features selected.

calculators

Explore the Power of Annuities in Your Retirement Plan

Discover how annuities can strengthen your retirement strategy with our easy-to-use calculators. See the difference tax-deferred growth can make compared to taxable investments, understand how tax advantages may amplify your savings, and get a clear estimate of how long your income could last in retirement.

These tools offer a helpful starting point, but a personalized strategy goes even further. Work with a financial professional to turn your insights into action and create a plan designed to support your goals for the long haul.

1 Annuity Guarantees rely on the financial strength and claims-paying ability of the issuing insurer.

2 2024 Read on Retirement survey | BlackRock

3 United Life Insurance Company does not offer variable annuities.

4 United Life Insurance Company does not offer registered index linked annuities.